Personal Finance

This channel is where we explore the holistic health of your financial house. Helpful, accurate articles include topics on credit, debt management, financial planning, real estate and taxes.

10 Types of Car Insurance Every Driver Needs to Know

5 Common Auto Insurance Scams (And How to Avoid Them)

How Auto Insurance Companies Work

10 Least Expensive States to Live In

What Are the Different Types of Life Insurance?

Do I Need Life Insurance?

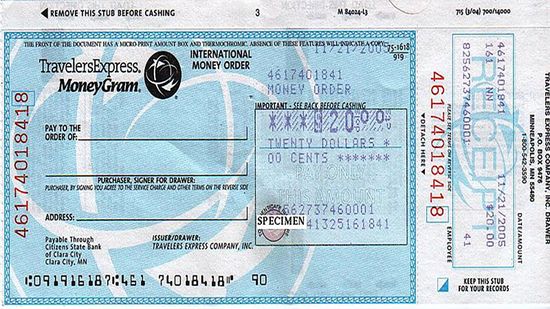

How to Fill Out a Money Order

How to Write a Check

How to Find Your Bank's Routing Number

Motel vs. Hotel: Differences in Overnight Accommodations

10 Things Hotels Don't Want You to Know

How Family Road Trips Can Be Done on the Cheap

How to Get Free Food While SNAP Benefits Are Delayed

11 Cheapest Halloween Candy Choices (and How to Shop Smart)

7 Best Chrome Extensions for Finding Coupons in 2023

5 Places That Will Pay You To Move There (Including 1 in Italy)

Can you use student loans to buy a used car?

What to Do When a Friend Owes You Money

How to Future-proof Your Child's Credit From Fraud

How to Avoid Being Evicted From Your Home

How Many Millionaires Are in the U.S.? More Than Any Other Country

8 Most Expensive Things in the World, From Parking to Palaces

Where Should You Put Your Money When Inflation Is High?

How Square Works

5 Ways Mobile Banking Alerts Can Benefit You

Is it safe to shop online with a debit card?

What's the Difference Between Student Loan Refinance and Student Loan Consolidation?

Is It a Good Idea to Refinance Your Student Loans?

10 Reasons College Costs So Much

9 Best Countries for Expats to Retire To

9 Pension-friendly States for Retirees

10 Tax-friendly States for Retirees

Does Dubai Have Taxes? Yes, Just Not Personal Income Tax

Cheapest Cigarettes by State: Where Average Cigarette Prices Haven't Skyrocketed

10 Crypto-Tax-Free Countries (and Where to Find 'Crypto Valley')

Learn More

Does Dubai have taxes? You might be surprised to hear that the answer is yes because Dubai is widely known as a tax-free destination for expats and international businesses.

When researching the best countries for expats to retire to, you may discover that moving abroad can stretch retirement income much further. Lower living costs, affordable health care, and welcoming expat communities often make retiring abroad financially realistic even with modest retirement savings.

If you are searching for the cheapest cigarettes by state, you need to know how state excise taxes and federal tax policy collide at the checkout counter. Cigarette prices vary widely across the country, with prices varying significantly from one state line to the next.

Advertisement

Want to keep more of your crypto gains? Then you're probably wondering about crypto-tax-free countries.

If you are researching the crypto-friendly countries, you are really asking where digital assets are legally supported, reasonably regulated, and taxed in predictable ways.

If you are looking for the pension-friendly states, you are really asking where retirement income is taxed the least and predictability is highest.

If you are researching the tax-friendly states for retirees, you are really asking how to stretch retirement income on a fixed income.

Advertisement

Looking for a fresh start and with financial incentives? These places that will pay you to move there offer relocation perks, remote worker packages, and community support to attract new residents.

Finding a place to live shouldn't cost your life savings. This list of the cheapest houses in the USA highlights cities and states where you can buy a home without spending millions of dollars (or in some cases, not even hundreds of thousands of dollars).

With a federal government shutdown disrupting SNAP (Supplemental Nutrition Assistance Program), nearly 42 million Americans have lost their food assistance and are turning to food banks and pantries for help.

Property taxes can feel like a second mortgage. But in some places, the annual bite is surprisingly small. These are the states with the lowest property tax rates, based on the effective property tax rate—the percentage of a home's market value homeowners pay each year.

Advertisement

Looking to keep more of your paycheck? Some U.S. states make it a lot easier. The states with the lowest taxes generally offer a friendlier environment for individuals and businesses alike, cutting back on income, sales, and property tax burdens.

Want to keep more of your paycheck? One way is to live in one of the states with the lowest income tax rates.

Property taxes may not grab headlines like income taxes, but they can take a serious bite out of your budget. So, which places hit homeowners the hardest?

We get it, you want the cheapest halloween candy without shortchanging the fun.

Advertisement

If your blood pressure is creeping up with your constant rent increases, you're not alone. With the rising cost of everything from groceries to gas, more Americans are looking for relief in the form of cheaper zip codes.

As of 2024, the number of millionaires in the U.S. was around 23.8 million. That means roughly 1 in 15 people in the U.S. has a net worth of at least seven figures. This number includes not just tycoons but also people who have slowly built wealth through investing, homeownership, and disciplined saving.

What’s the most expensive city in the U.S.? The answer depends on how you calculate cost, but some major cities stand out for their soaring living costs, housing prices, and everyday expenses.

Understanding the different types of car insurance is crucial to getting the right coverage for your vehicle, your budget and your peace of mind.

Advertisement

Luxury real estate isn’t just about square footage and designer finishes; it's also about location. The 10 most expensive zip codes in the U.S. reveal where affluence concentrates, with sky-high median sale prices and jaw-dropping properties.

For residents of certain states, the absence of a state income tax can be a significant tax benefit. Instead of paying personal income tax rates to the state, individuals in these states only pay federal income tax on their taxable income.

By Mack Hayden

The last Mega Millions jackpot paid roughly $50 million in cash, though many jackpots in recent history have exceeded the billion-dollar mark. With potential windfalls reaching those extreme levels, it's easy to see why so many people play each week.

By Mitch Ryan

The latest technology has often improved daily life, making many problems faster and easier to solve. For example, you may have built your own Batcave-like command center with multiple monitors, each equipped with a customized browser to view each day's weather broadcast, news and work emails.

By Mitch Ryan

Advertisement

Temu, the ultra-affordable online marketplace taking social media by storm, is having a huge moment. But while it's become the go-to spot for incredible deals, the retail site is also a magnet for scammers looking to cash in on the buzz.

Facebook Marketplace has become a popular platform for buying and selling goods, from used cars to gaming systems. However, as with any online marketplace, it has also become a breeding ground for scams.

By Marie Look