Starting a company entails understanding how the business legal structure works. Sam Edwards / Getty Images

You are starting a company and want to limit your personal liability for the debts of the business as well as the taxes you'll have to pay. This is a common goal for many new business owners. Having a good understanding of how business legal structures work, however, is not so common. So, what are legal structures and what type(s) should you consider? C-corporations, S-corporations, limited liability companies, sole proprietorships, and partnerships are some of the more common options for business legal structures. There are differences and similarities in each that can dramatically affect the future of your company. Failing to structure your business in the most appropriate way (given your goals) can lead to many bad outcomes including:

Higher than expected tax payments

Large amounts of administrative work and costs

Unexpected loss of your personal assets.

In this edition of HowStuffWorks, we will look at each option and help you make sense of the details so you can select the right structure.

Why should I care about business legal structures?

Think about what can happen when you start your business. In a simplified way, there are two scenarios. One scenario is that your business will be a success and profitable. The other scenario is that your business will fail and lose money. By setting up your business structure correctly, you will be better off in both scenarios. The flip side of that is also true; by not setting up your business structure correctly, you will make yourself worse off in both scenarios.

So, if it is so important to set up a business structure correctly then why isn't there more straightforward information on the topic? Most likely, the lack of information stems from the multitude of structures available and the nuances of each. Even entrepreneurs who study the details of each type of structure are often left confused with information overload. Therefore, while setting up your business structure is not one of the most sexy aspects of starting a business, it can indeed end up being one of the most important.

Advertisement

Key Issues of Business Legal Structures

There are three key issues that differentiate the various types of business structures. By understanding these core issues first, you will be able to understand the advantages and disadvantages of each type of structure.

Taxes

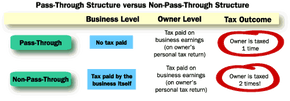

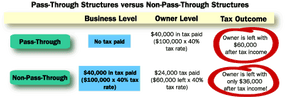

How many times will I pay tax?

Advertisement

That's right - it's not a matter of if you will pay tax, but rather how many times will you pay tax. Certain structures are called pass-through entities, and the income and losses are literally passed through from the business to the individual for tax purposes. Other structures form a separate tax entity that is taxed by itself. Then, when earnings are distributed, the owner is taxed again on that business income.

Quite simply, you may not end up with the amount of money you think you will be getting. Look at the following example to see the difference in after-tax money that the owner receives.

The following numerical example shows how this issue can make a big difference in after-tax income to the owner, (which is what most business owners are mainly concerned about.) Assume the owner had a business that made $100,000 in the past year, and that the tax rates for business and individuals are 40%.

Using similar logic, it is important to note that many businesses will have losses in early years and that owners can obtain significant tax advantages by having these losses passed through to their personal income tax returns. The net effect will be less tax paid by the owner, thereby leaving him with more after-tax income.

Liability

Who is responsible for the debts and liabilities of the business? If you drive your car into another car, then you are liable for damages. Who is liable for the possible damages and debts incurred by your business? It depends on the type of structure. Some structures will limit your liability to your investment, whereas others will make you and your personal possessions liable for the damages and debts of the business.

You could lose everything you own in your business and in your personal possessions. This means your car, your house, your personal bank account and more. Your business can incur damages in any number of ways. For example, if you end up going bankrupt and still have outstanding bills, the creditors will come after your personal assets. Also, if a driver for your company accidentally kills a pedestrian, your business can become liable. Depending on the business structure, your personal possessions may also be at risk.

For example, Bob Smith's lawn care business has gone bankrupt. Unfortunately for Bob, his company owes a supplier over $10,000 for equipment that he had purchased several months ago on installment. The company no longer has the funds to pay off the debt, and is structured in a way that makes Bob personally liable for the debts of his business. The supplier takes actions against Bob's personal assets to recover the $10,000.

Administrative Costs

How much time and money will it cost to set up and run my business under this structure?

How much time, effort, and money will it cost you to set up and run the company? Some structures are very costly in this sense while others are relatively low maintenance.

While the first two issues (taxes and liability) are more important overall, administrative costs should not be overlooked. The costs of both money and time can be cumbersome, especially for a startup with fewer resources. These expenses include tax-filing requirements, complexity of startup documentation with appropriate agencies (i.e. articles of incorporation), and both federal and state laws dictating necessary behaviors of the business.

Bob Smith sets up his business as a structure that is extensive in its administrative costs. The set up alone costs Bob several thousand dollars and periodically Bob is required to hire an accountant to fill out paperwork and forms for several government agencies. All in all, these administrative procedures take up a good amount of Bob's time and money.

Advertisement

Types of Business Legal Structures

Now let's talk about the basic advantages and disadvantages of each type of structure.

Sole Proprietorship

Simple Definition

A legal form of business that makes no legal distinction between the individual owner and the business itself.

Advertisement

Advantages

Administrative setup and maintenance costs are low

Relatively few regulatory requirements

Owner is only taxed once on his or her personal income tax return

Disadvantages

Owner is personally liable for the actions of the company

Can be difficult to raise capital for the business

Other comments

Typically the sole proprietorship is set up as the owner's name (e.g. Bob Smith). The owner can choose to operate his or her business under a different name (e.g. Smith's Lawn Care) but then must file a doing business as form with the appropriate government body.

It is possible to self-insure yourself against the personal liability assumed by this structure.

General Partnership

Simple Definition

Similar to a sole proprietorship but with multiple owners (a sole proprietorship cannot have more than one owner). Like a sole proprietorship, a partnership is not a separate legal entity from its owners.

Advantages

Administrative setup and maintenance costs are low

Relatively few regulatory requirements

Owner is only taxed once on his or her personal income tax return

Disadvantages

Owner is personally liable for the actions of the company

Each partner is responsible for the business dealings of other partners. This is very important to understand. If Partner A enters into a very bad deal under the name of the partnership, then all other Partners are responsible for making good under that contract. Consequently, selecting your partners is of crucial importance.

Other comments

The partnership agreement is the rule book of the partners. This can be drafted with the help of a qualified lawyer to help the partnership deal with such issues as:

Initial investment of partners

Distribution of profits and losses

Each partner's responsibilities

New partner entrance into partnership

Old partner exit from partnership

Limited Liability Partnership

Simple Definition

Similar to a general partnership but with a separate classification of partners (see Other Comments section below for further explanation).

Advantages

Owner is only taxed once on his or her personal return

Liability can be limited (for limited partners see other comments below)

Disadvantages

More complex filing and administrative requirements than a general partnership

General partners still have personal liability - makes sense if there are numerous passive investors who wish to limit their liability.

Other comments

As opposed to a general partnership, a limited liability partnership has two kinds of partners, general and limited. General partners are similar to those in general partnerships they operate the business and assume liability. Limited partners, on the other hand, are merely investors and, therefore, have no control or operational power. They do have limited liability.

C-Corporation

Simple Definition

A legal form of doing business that creates a separate legal entity from the individual owners. This legal entity can act and do business on its own just as a person would do (i.e. borrow money, enter into lawsuits and contracts, etc.).

Advantages

Shareholders are not personally liable

Ownership is easily exchanged between individuals

Company does not cease to exist with the death of owners

Easy structure for which to raise capital

Disadvantages

Owners are taxed twice

High administrative costs to setup and run

More regulatory requirements than other structures

Other comments

It is important to remember that a C-corporation is considered a separate legal entity from its owners. This is the source of its relative advantages and disadvantages, especially regarding taxes and liability.

S-Corporation

Simple Definition

A type of corporate legal form that is taxed like a sole proprietorship. Its formation is subject to certain legal criteria such as a maximum number of shareholders.

Advantages

Owners are only taxed one time. Shareholders are not personally liable

Disadvantages

Higher administrative costs to setup and run than partnerships and sole proprietorships. More regulations than partnerships and sole proprietorships. Certain limitations on who can be an owner (U.S. citizens, etc.)

Other comments

S-corporations are limited to a certain number of shareholders (75), whereas a C-corporation can have unlimited shareholders.

Limited Liability Company (LLC)

Simple Definition

A hybrid legal form of business that is taxed like a sole proprietorship with the same liability protection of the corporate structure.

Advantages

Owners are only taxed one time. Shareholders are not personally liable

Disadvantages

Higher administrative costs to setup and run than partnerships and sole proprietorships

More regulations than partnerships and sole proprietorships

Limited life of entity (usually limited to 30 years)

LLC laws are not uniform and therefore doing business in multiple states as an LLC can be complex

Other comments

The L.L.C. is an extremely popular structure. Since there are many similarities between LLCs and S-corporations, the list below shows some of the differences:

LLC relative advantages over S-corporations:

No restrictions on the number of owners (S-corps limited to 75 owners)

Can have non-U.S. citizens as members (S-corps cannot)

More flexibility in distributing income (S-corps percentage of ownership determines the amount of pass-through income)

LLC relative disadvantages over S-corporations:

Need at least two people to form an LLC (S-corps only need one person)

Limited life (S-corps are perpetual)

LLC members need other members' approval to sell their interest (S-corps owners need no such approval)

LLC may have to pay more self-employment taxes than S-corps due to IRS regulations forcing active LLC members to pay self-employment taxes on both salary and distributions from the company, as opposed to S-corps members who do not have to pay taxes on distributions.

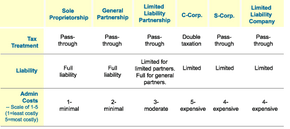

The key factors that differentiate structures are summarized in the chart below:

Advertisement

Assess Your Business's Legal Situation

Next, you should assess your own personal situation in relation to the types of structures. How much in taxes am I willing to pay? How much liability am I willing to assume? Will administrative costs become too much of a burden on me? These questions should all be answered together as there is no one perfect structure for everyone.

Thinking through the key issues will help you to logically select the appropriate structure given your situation. (As a quick note, many early stage businesses are currently being structured as L.L.C.s due to their advantages of pass-through income and limited liability).

Advertisement

Professional Legal Help for Businesses

Before actually deciding on your structure, seek the advice of an accountant or lawyer with specialized knowledge in this area. There are numerous federal, state, city, and local laws that you should be aware of depending on your location and the type of business you are running. Some of these laws may require special filings or permits to be obtained before you can open for business. A lawyer or accountant can help you to sift through the final layer of detail before you set up your business.

Advertisement

Business Legal Structures: Conclusion

Here is a simple checklist to complete as you begin to set up your business structure:

Understand the main differences between business structures (taxes, liability and administrative costs)

Understand the relative advantages and disadvantages of each type of structure

Assess your own desires and determine which structure is right given your situation and type of business. Li>Seek professional help to ensure that you are not overlooking any details (city permits, licenses, etc.).

Remember, setting up your business structure is not the most exciting part of starting your business, but can be a burden if you fail to select the best structure. Take the time to work through the above checklist and you will protect yourself against being unpleasantly surprised in the future.