The National Automated Clearing House Association (NACHA), also known as the Electronic Payments Association, has helped increase the use of e-payments and e-checks. NACHA governs the nationwide Automated Clearing House (ACH) network. Through this network, NACHA's 11,000 member banks and other financial institutions offer direct deposit, direct debit and e-checks for consumers and businesses.

That activity is fairly invisible as you check bank account balances online, make purchases from online stores with a debit card or pay bills from your bank's Web site. But NACHA's role is an important one. The not-for-profit association develops operating rules and business practices for the ACH network to make sure it stays efficient, reliable and secure -- keeping your electronic payments that way, too.

NACHA also offers tools and resources to help its member institutions facilitate electronic payments. And the association develops electronic payment practices beyond the ACH network for areas like Internet commerce, financial electronic data interchange (EDI) and international payments [source: NACHA].

As one of its services, NACHA tracks the growing use of electronic payment through quarterly and annual reports. For example, the ACH network handled nearly 16 billion payments totaling $30.3 trillion in 2006, a 14.5 percent increase over 2005, according to NACHA statistics. That includes payroll direct deposits, Social Security benefits, tax refunds, payment of 8 billion consumer bills and more. The rate shows that the volume of electronic payments continues to double every five years [source: NACHA].

While most of NACHA's offerings are targeted to its member financial institutions, the association offers help for consumers and small businesses through an interactive Web site.

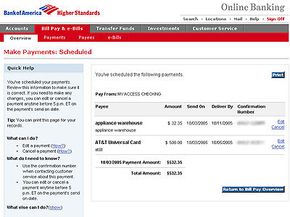

On the Web site, you can watch virtual demonstrations of how direct deposit, direct payment and check conversion work. You'll also find explanations of the different types of electronic payment along with information on how to decide whether payroll direct deposit and direct payment of bills are good options for you.

The Web site's business section provides a cost benefit analysis of direct deposit and direct payment for businesses of different sizes, marketing tool kits for businesses' employees and customers, and suggested answers to customer questions about check conversion [source: NACHA].

Through its Pay It Green initiative, NACHA is encouraging consumers to receive and pay bills electronically instead of on paper to save trees, fuel and water. The alliance brings together NACHA, the U.S. Federal Reserve, and leaders of the financial and consumer billing industries.

The initiative cites a 2007 survey by Javelin Strategy and Research indicating that if all U.S. households received and paid their bills electronically, the United States would:

- Save 16.5 million trees every year, providing enough lumber for 216,054 single-family homes

- Reduce toxic air pollutants by 3.9 billion tons of carbon dioxide equivalents, the equivalent of taking 355,015 cars off the road

- Reduce by 1.6 billion pounds the solid waste generated each year by 1.6 billion pounds, the weight of 56,000 fully loaded garbage trucks

Paper isn't the only item consumed through traditional bill paying, the alliance points out. The group is developing tools and resources that show the environmental benefits of choosing electronic options over paper [source: NACHA Pay It Green].

For lots more information about electronic payments and related topics, check out the links on the next page.