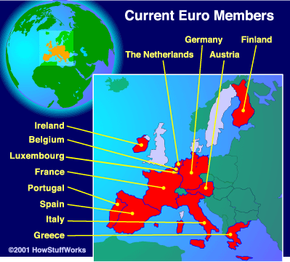

The Treaty of Rome was ratified in 1958, establishing the European Economic Community (EEC). The goal of the EEC was to reduce trade barriers, streamline economic policies, coordinate transportation and agriculture policies, remove measures restricting free competition, and promote the mobility of labor and capital among member nations. It was very successful, but just as with the ECSC, it served more of a peacemaking role between the European nations than an economic role.

At this time, the monetary exchange rate between countries was controlled by the Bretton Woods system, which connected currencies to the U.S. dollar, allowing for only a one point fluctuation around designated values. This was referred to as the "pegged rate" and was based partly on the gold backing of the dollar. This system worked well for 20 years, helping to stabilize exchange rates and restore economic growth in the postwar period. By 1960, however, the system began to fail, and exchange-rate agreements became the prevalent topic among European political and economic leaders.

By December 1969, Luxembourg's Prime Minister, Pierre Werner, was asked to write an EC (European Community) report covering the need for a complete monetary union among the European economies. The Werner Report came out in 1970 and specifically brought up the idea of a single European currency as part of a cooperative monetary effort. The report was the first to use the term Economic and Monetary Union.

Although this plan seemed promising, it lost momentum when President Nixon's 1971 policy of "benign neglect" ended U.S. backing (by its gold reserves) of the predefined exchange rates against the dollar, collapsing the Bretton Woods system. Other foreign central banks were not willing to support the dollar, which would have provided the equivalent of deposit insurance.

So where did that leave the European countries when it came to the stability of their currencies? It brought about the development in 1979 of the European Monetary System (EMS), which locked exchange rates among the participating countries into predefined trading zones. This was known as the Exchange Rate Mechanism (EMS). This move, in itself, stabilized the economy by creating predictable trading zones.

The next move toward a unified European economy came with the 1987 Single European Act. This act called for the systematic removal of barriers and restrictions that hampered trade between European countries. As a result, border checks, tariffs, customs, labor restrictions and other barriers to free trade were dismantled.

For more information on the euro and related topics, check out the links on the next page.