Banks are now customizing mobile banking services with customized software.

Banks are now customizing mobile banking services with customized software.Although several financial institutions, including Wachovia, Washington Mutual, Wells Fargo and ING Direct, are launching mobile banking services, we are going to look at two of the largest and most developed -- Mobile Banking from Bank of America and Citi Mobile from Citibank.

Mobile Banking from Bank of America

Bank of America chose wireless application protocol as its technology platform. That means any cell phone with Web access can use the service -- without downloading any software. However, any customer who wishes to use the mobile banking services must be set up in online banking. That’s because all transfer and payee information must be set up on a PC prior to making payments or transfers in Mobile Banking. Once these criteria are met, customers can:

- Access their checking, savings, credit card, mortgage, line of credit, loan and other Bank of America accounts

- Pay bills anywhere, anytime

- Transfer funds from one Bank of America account to another

- Locate branches or ATMs

- Get maps and directions

Bank of America advertises its Mobile Banking as free, but that doesn’t mean customers won’t incur costs. They will be charged access rates depending on their mobile carrier. Those who wish to use mobile banking regularly will be better off signing up for a data plan providing a certain allotment of data and text messages for a monthly fee. Such a plan is likely more cost-effective than paying for several one-off charges.

Citi Mobile from Citibank

Citibank opted for the application-based approach to its mobile banking offering. Like Bank of America Mobile Banking, Citi Mobile requires that users spend some time on a PC getting the service set up. Citi Mobile customers must also download software -- a custom, Citibank-branded interface -- to their phones. Here’s how the process works:

Citibank customers sign on to their online banking accounts and enter their cell phone numbers, the name of their wireless carriers, and their cell phone models. This information is necessary because the Citi Mobile application must be customized to the make and model of the phone.

After customers enroll, two text messages land in their cell phone inbox: The first with download instructions and the second with an activation key, which is required to set up the application on the phone.

Customers download and install the application to their phone, a process that takes about two to three minutes.

Next, customers launch the application and enter their activation keys and cell phone numbers to initiate the mobile banking service. They're ready to sign on. Every time they sign on, customers will need to enter their telephone access codes -- the same code they use to access Citibank’s telephone banking service.

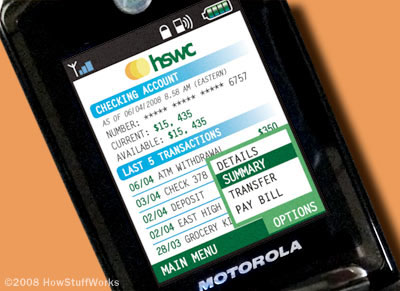

The Citi Mobile interface provides access points into account information and activity, payments and transfers. It also allows users to find Citibank locations and to connect to customer service with a single click.

Citibank is looking to push the boundaries of mobile banking with some innovative cell phone trials. One trial, a partnership with MasterCard, AT&T and Nokia, involves placing near field communications (NFC) chips in certain Nokia phones. By passing the phone within a few inches of a reader, the NFC chip can be used to charge a payment to the user's credit or debit card. Such a payment is called an m-payment, an exciting concept in the world of mobile banking.

M-payments will be possible even when the phone’s user doesn’t have a bank account. In such a situation, a cell phone owner buys prepaid units from a mobile operator and then uses those units to pay for goods and services at a partnering service provider or retailer. Some see this type of transaction as a vital way to get basic financial services to populations in developing countries or in rural or remote areas, where people are more likely to have cell phones than bank accounts.

So perhaps a future commercial for mobile banking will not show an American woman hanging from a cliff in the Utah badlands, but a Kenyan villager using her cell phone to make a money transfer in downtown Nairobi.

For more information on mobile banking and related topics, see the links on the next page.