Checking Accounts

Banks offer lots of financial products for their depositors. The checking account is one of the most common ones. It's convenient because it lets you buy things without having to worry about carrying the cash -- or using a credit card and paying its interest. While most checking accounts do not pay interest, some do -- these are referred to as negotiable order of withdrawal (NOW) accounts. Some say that checks have been around since about 352 B.C. in the Roman Empire. It appears that checks really started becoming popular in Holland in the 1500 to 1600s. Dutch "cashiers" provided an alternative to keeping large amounts of cash at home and agreed to hold depositors' money for safekeeping. For a fee, they would pay the depositors' debts from the account based on a note that the depositor would write -- sounds a lot like a check!

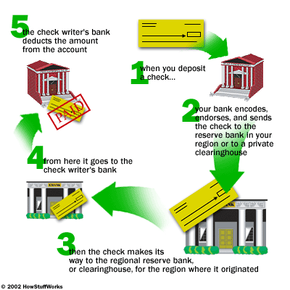

Today's banks do the same thing. It became a little more complicated when lots of banks became involved and money needed to be shifted from one bank to the next. To make things easier, banks now have a system of check "clearinghouses." Banks either send checks through the Federal Reserve or use a private clearinghouse to transfer the funds and clear the check. Here is a diagram of how that works.

Advertisement